Caledonia Mining is to decide by year-end whether to build the Bilboes project in phases – potentially halving the original plant size to curb equity dilution and limit financial risks, CEO Mark Learmonth says.

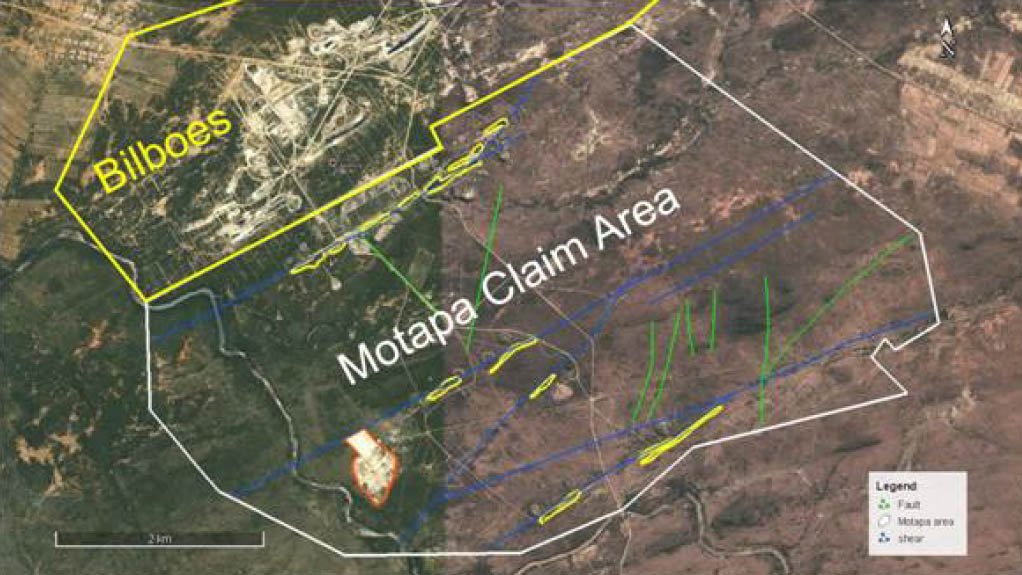

The May 2024 preliminary economic assessment (PEA) outlined a 10-year operation averaging about 150,000 oz. gold annually at an all-in-sustaining cost just under $1,000 per ounce. Bilboes, which would supplement the company’s producing Blanket mine in the country’s southwest, hosts about 33.7 million tonnes measured and indicated at 2.3 grams gold per tonne for 2.5 million oz. of metal.

“We’re updating that PEA to reflect the current environment but we’re also looking at how we can digest this asset in a phased basis, with a way of minimising or avoiding equity dilution and reducing what I call financial jeopardy,” Learmonth says. “This is a big, big project for our company. We get one chance to get it right.”

Improving jurisdiction

Zimbabwe ranks low in most global mining perception surveys, but capital is flowing into the country and the wider region as operators chase scale and battery-metal exposure. Platinum major Zimplats has kept spending through the cycle, with more than $300 million pushed into mine replacements, smelter and sulphide projects in the past 12 months. Chinese-backed Tsingshan brought a $1 billion steel plant online last year aimed at downstream demand.

In lithium, policy is tilting to in-country value addition – Zimbabwe will ban lithium concentrate exports from January 2027 – underpinning a wave of Chinese investment exceeding $1 billion since 2021 and new plants such as the $310 million build–operate–transfer concentrator at state-owned Kuvimba’s Sandawana site.

Investor sentiment on Zimbabwe is rebounding from multi-year lows, management argues. Learmonth described a more predictable policy environment and fewer “scary moments,” while noting that relative risk across several African peer countries has risen. Caledonia’s established operating footprint at Blanket and local know-how are flagged as competitive advantages in a bureaucratically complex jurisdiction.

Shares of the company have more than doubled in New York trading in the past 12 months to $36.55 as of Thursday afternoon. Caledonia has a market capitalisation of $705 million.

Stepped approach

A smaller first phase for Bilboes – around 120,000 tonnes per month – could still double group output from today’s levels and create a self-funding springboard to the second-stage operation once cash flow generation has begun, Learmonth said.

That approach may also shorten the time to first gold in a volatile cost environment without sacrificing long-term scale. Caledonia bought Bilboes in January 2023 for about $65.7 million in shares. “A smaller starter project will be materially cheaper and therefore easier for us to fund with less recourse to equity,” Learmonth said. Bilboes ore is refractory and BIOX processing is planned.

The board expects to settle on a development approach by year-end. If Caledonia proceeds with a full-scale build, management expects to publish a conventional feasibility study. A phased start would require additional technical work and could prompt the company to skip publishing a feasibility study. In both cases, the goal will be to increase the net present value per share by balancing growth, conservative leverage and continue paying dividends.

Caledonia’s stance on shareholder returns remains a central constraint on how Bilboes is to be financed. Caledonia’s strategy over the past decade has been built on “minimising dilution” and paying a regular dividend, Learmonth said. Cutting the dividend to fund growth is not part of the plan.

“Those two disciplines are deeply embedded in our DNA,” he said. Blanket continues to underpin group cash generation. Production has stabilised between 75,000 and 80,000 oz per year, with management shifting attention from growth to cost control, notably electricity and labour.

Power reliability is a key lever on unit costs. About 20% of Blanket’s demand is met by solar, with the balance tied to an unreliable 33-kV grid link that forces periodic diesel use. Diesel power costs the operation roughly $0.45 per kWh, versus about $0.12 per kWh for grid and a similar blended rate for solar.

To cut outages and diesel burn, Caledonia plans to connect to the country’s 132-kV network – an upgrade pegged at about $10 million – opening access to cleaner regional imports from Mozambique and Zambia. The company has already sold its on-site solar plant to CrossBoundary Energy and is redeploying capital elsewhere, while retaining power supply via contract.

“We’re going to triple the size of the company based on growth, yield and a reappraisal of Zimbabwe,” Learmonth said. – (mining.com)